Almost every couple of years, the world has faced a new 'apocalypse', and for each one we have rightly wondered and worried how these larger global rumblings might affect us in Jamaica. This was true for the millennium bug, the tsunami disasters, the ongoing issue of climate change, and it is once again true for the financial crisis that the world presently finds itself in the grip of.

But the world hasn't ended yet and at CaPRI (Caribbean Policy Research Institute) we are reminded of the original definition of apocalypse - not a cataclysmic destruction at all, but a time when things once done in 'secret' are finally revealed. The inner workings of the global financial sector have indeed been a great secret to most people, and though the present crisis constitutes the greatest economic challenges we have faced since World War II, it is still as good an opportunity as any to do some re-evaluating and repositioning.

The financial crisis comes with a whole new vocabulary for those of us with less financial savvy to learn: words like subprime, credit-crunch, mortgage-backed-securities, among others. In this series of articles, CaPRI will attempt to navigate through this new language, and also will suggest how Jamaica might navigate its own way through this 'apocalypse'.

Subprime mortgages

The subprime market is a concept that the average Jamaica is already familiar with, even if not by that term. The 'hire purchase' products favoured by large furniture and appliance stores have for a long time tapped into this demographic. Put in the best possible light, one might say subprime mortgages represented an attempt to make the American Dream obtainable to under-privileged and minority groups that otherwise could not have achieved it.

In the housing boom of the mid-'90s, several people in America found they did not meet the strict criteria needed to obtain a loan. The reasons varied: the loan-seekers either had a bad credit history, or they were under-employed, or they had been victim of a personal financial crisis - divorce, illness, etc. With low interest rates, there was a high demand for mortgages, but the banks' doors remained closed to them. They were not 'prime' candidates for loans or mortgages - instead they were 'sub-prime'.

The banks, however, recognised that by tapping into this swelling subprime market they could make a tidy profit. They did this by charging higher interest rates to poorer people. The justification was this: the banks were taking a much larger risk in handing out loans and mortgages to people who were five-and-a-half times more likely to default on them. In the case of the American housing market, hindsight suggests that the risk of default, and its impact, were in fact much greater than the banks anticipated.

Worldwide crisis

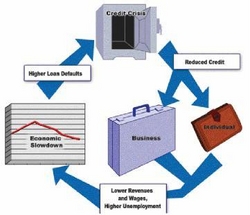

But how did this situation of sub-prime mortgages catapult into a worldwide crisis that has real implications for Jamaica now? The subprime market ballooned before it burst. It grew significantly between 2004 and 2006 - where about 2,500 banks, credit unions and mortgage companies accounted for US$ 1.3 trillion in high-interest rate loans, according to the Wall Street Journal. The real crisis, however, began to precipitate when these mortgages were 'securitised'. Securitisation is yet another concept the less financially astute among us have had to learn. Financial institutions, instead of holding on to their risky loans, turned them into assets and sold them. On one hand, it meant they got less of a payback than if they had held on to the loan or mortgage for its full term, but on the other hand - they let go of their risk, they got back their investment, and had new cash to spend and reinvest. The situation became international when these risky subprime mortgages were then repackaged in this process of securitisation, given AAA ratings, and sold internationally to countries like Japan, China and Russia, as low-risk products. Pension funds and government investors around the world bought into them.

The bubble burst. With high interest rates and an increasing number of defaults, the subprime market began to show signs of its impending collapse, and then in April 2007, New Century Financial, the second largest lender of sub-prime loans, filed for bankruptcy. It was followed in quick succession by several other major financial institutions.

Dramatic reversal

In a dramatic reversal, banks which had previously relaxed their regulations and had been giving credit less scrupulously than one would have hoped, now became very suspicious and started to hold on to their money. It has now become the era of the credit crunch. Loans and mortgages, once easily attainable, are now exceedingly difficult to secure.

How the 'apocalypse' could affect Jamaica

Like all impending storms, it is impossible to predict exactly what damage will occur. It is enough, however, to keep our heads out of the sand, make intelligent guesses as to what the possible fallouts could be, and to brace ourselves for them. The Jamaican economy will not be spared the effects of the crisis and, indeed, has already begun to experience some of its repercussions. Already, remittances are down by 18 per cent. While admittedly only a few local financial institutions have been directly affected by virtue of their investments in American institutions to the crisis there, if the global credit crunch and recession persists, Jamaica will soon face other serious challenges.

Possible challenges

1. If Government of Jamaica (GOJ) Treasury Bills lose value, Jamaican financial institutions will also experience deterioration in their asset bases, though this is only likely to raise issues of solvency if the Jamaican government defaults on its obligations.

2. The Government might experience difficulties in raising money on the international market. This has serious implications for our ability to meet obligations locally and externally, and to undertake big expenditures such as Highway 2000.

3. Jamaica may also have to deal with declining exports. Consumer confidence is the lowest it has been in almost 30 years in America, and import prices fell by 4.7 per cent in October 2008. So Jamaica's export revenues are likely to be adversely affected by declining volumes and prices.

4. Job losses in America, Canada and the UK may have begun to affect remittances to Jamaica. These inflows must be carefully monitored, especially in light of the probability of a prolonged global recession.

5. Tourism is vulnerable. Although falling oil prices should reduce the cost of airline tickets, the income effects of the credit crunch may force US citizens to seek cheaper vacation alternatives.

Producers may see one significant opportunity in all of this, and use this crisis as a perfect time to diversify away from an over-reliance on the American market. And, for consumers and importers, declining prices on oil and other products are certainly not all bad news. Jamaica may also see this as an opportunity to control domestic inflation and improve financial awareness and regulation.

The Caribbean Policy Research Institute (CaPRI), is an independent think tank affiliated to the UWI, Mona. CaPRI welcomes all comments and suggestions. Please contact us at info@capricaribbean.org.