Wilberne Persaud, Financial Gleaner Columnist

Committed ideologues, left or right, are scary. America's extreme right denies diversity in a world they inhabit; diversity, which by the way, is its true strength.

It is its strength whether as process, natural selection among animals and plants, or human populations and cultures across the planet.

Today the extreme right's endless reliance on stale talking points, defense of the indefensible and a fringe, intellectually though not by virtue of its huge listenership on United States talk radio, actually blame Barack Obama for Wall Street's profligacy though he is merely president-elect, innocent bystander.

Freedom of speech is fine. Recasting Mao's vision of ideas contending, we can change 100 flowers blooming to 1,000 voices booming!

The real problem arises if somehow those voices influence US policy in tackling what can be not the great, but the greatest depression.

Say's Law

In 1929, economists were still wedded to Say's Law: supply creates its own demand. This was accepted just like 'at sea level, water boils at 100 degrees'.

Problem is Say's Law was untrue. The theory was flawed.

Economic theory did not admit the possibility of involuntary unemployment. People could remain unemployed only if they abandoned the labour market.

There could be no unmet demand alongside idle industrial plant and human labour. That was hogwash which happily, empirical reality jettisoned.

Soup lines of ill-clad adults, mostly male but with some females too, alongside idle factories, cannot be ignored even by the extremists.

Yet, as one reads John Maynard Keynes' 1936 General Theory, one can't but be struck by the enormous effort he makes describing, and justifying, his break with orthodoxy.

His break with the brotherhood Ś and brotherhood it was, for there was only one woman in the firmament of economists, Joan Robinson at Cambridge Ś he happily associated and identified with for most of his adult life was difficult.

He introduced the consumption function, savings being equal to investment but not in the sense of expectations of business selling output as opposed to consumers saving for a rainy day.

Concepts of national income we now take for granted with aggregates collected and published annually by the United Nations system became possible as these ideas developed.

He also introduced the idea of a liquidity trap Ś a kind of pushing on a monetary string, or taking horse to the water but being unable to make it drink.

Give banks money yet they cannot lend because business borrowers are fearful.

Our understanding, or rather lack of understanding prior to this, of how the real and monetary economy worked made it impossible to respond proactively to the great crash of 1929. Policy or inaction combined with circumstances to deepen the meltdown.

Today is different.

Decision process

We know much more about how the economy really works, how human decision taking responds to conditions and expectations formed about economic reality and anticipated behaviours of competitors, allies or partners and an enabling government in the capitalist profit making enterprise.

This knowledge allows us to choose policy that stand the chance of avoiding meltdown into depression.

But for instance a McCain advertisement this year claimed: "Higher taxes, more government spending, so fewer jobs"; Rush Limbaugh, the popular, unapologetic extreme right wing radio talk show host, claims that "the government can't create wealth; it can only destroy it or confiscate and redistribute it."

These notions are, perhaps not surprisingly, taken as self evident truth by over 30 per cent of the American population Ś amazing but true.

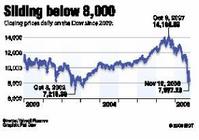

This base then provides the backbone of opposition to government intervention, on ideological grounds, to rescue the economy. Hence the initial failure of the Henry Paulson requested bailout bill and its implementation in perhaps the worst way possible for its success.

The core crisis is the bottom falling out of the housing market.

Should that bottom be supported, and the only way to do that is target homeowners in distress, the length and perhaps spread of the crisis will be reduced.

This has its hazards but no more than a non-transparent bailout of Wall Street with little that is truly positive to report. Of course, while we cannot say, perhaps much that is negative may already have been avoided.

Foreclosures affect whole neighbourhoods, and distressed as well as currently paying mortgage holders, causing lenders to lose much more that they would by partial debt forgiveness.

All property values plummet.

Vandalism generally intervenes and distressed borrowers cease being effective consumers.

Add to this, potential loss of one in every 10 US jobs related to the auto industry and this recession shall become a depression which will last several years before it turns upward.

Big trade and fiscal deficits

Here's the problem Ś the US has big trade and fiscal deficits while pursuing two wars spending billions.

Its financial services sector has allowed greed, euphoria and a regulatory system that makes a casino seem over-policed, to create a global bubble gone into meltdown.

The United Kingdom has a similar situation. Europe, though not as bad is stumbling.

Global reach of the US meltdown encompasses players as far away and as small as Iceland, allowing Reykjavik's woes to have a mushroomed financial crash impact.

So we can look at the US economic system as needing 'foreign exchange' support. There is no International Monetary Fund (IMF) programme, no standby arrangement it can sign on to. The US is the IMF.

It gets support from China, Saudi Arabia, Japan and so on Ś countries that accumulate surplus dollar holdings partly through consumer saving partly through sovereign funds.

Hodgepodge arrangement

But this hodgepodge arrangement cannot stand. Markets keep telling us that.

Participants are uneasy in New York, Hong Kong, Singapore, Australia, London Ś in effect the globe.

So Nicolas Sarkozy proposes and George W. Bush approves the G-20 summit.

In the Bush lame duck period little can be accomplished. Yet the mere fact of convening such a meeting is an important first step.

The time is ripe now for more equitable sharing of benefits, responsibility, and sacrifice the world economic system places upon different countries and peoples.

Squabbling over European 'socialist' practice, thoughts of American capitalism's demise countered by right wing ideology are entirely counterproductive.

Rome is already burning. Fire trucks are close to hydrants. How long will water remain in the pipes?

wilbe65@yahoo.com